How Employee Tax is Calculated

Employee Tax is calculated on the Annual income of an employee. Annual income means income received by an employee for a financial year starting from Shrawan 2083 to Ashadh 2084. The income is taxable on right to receive basis.

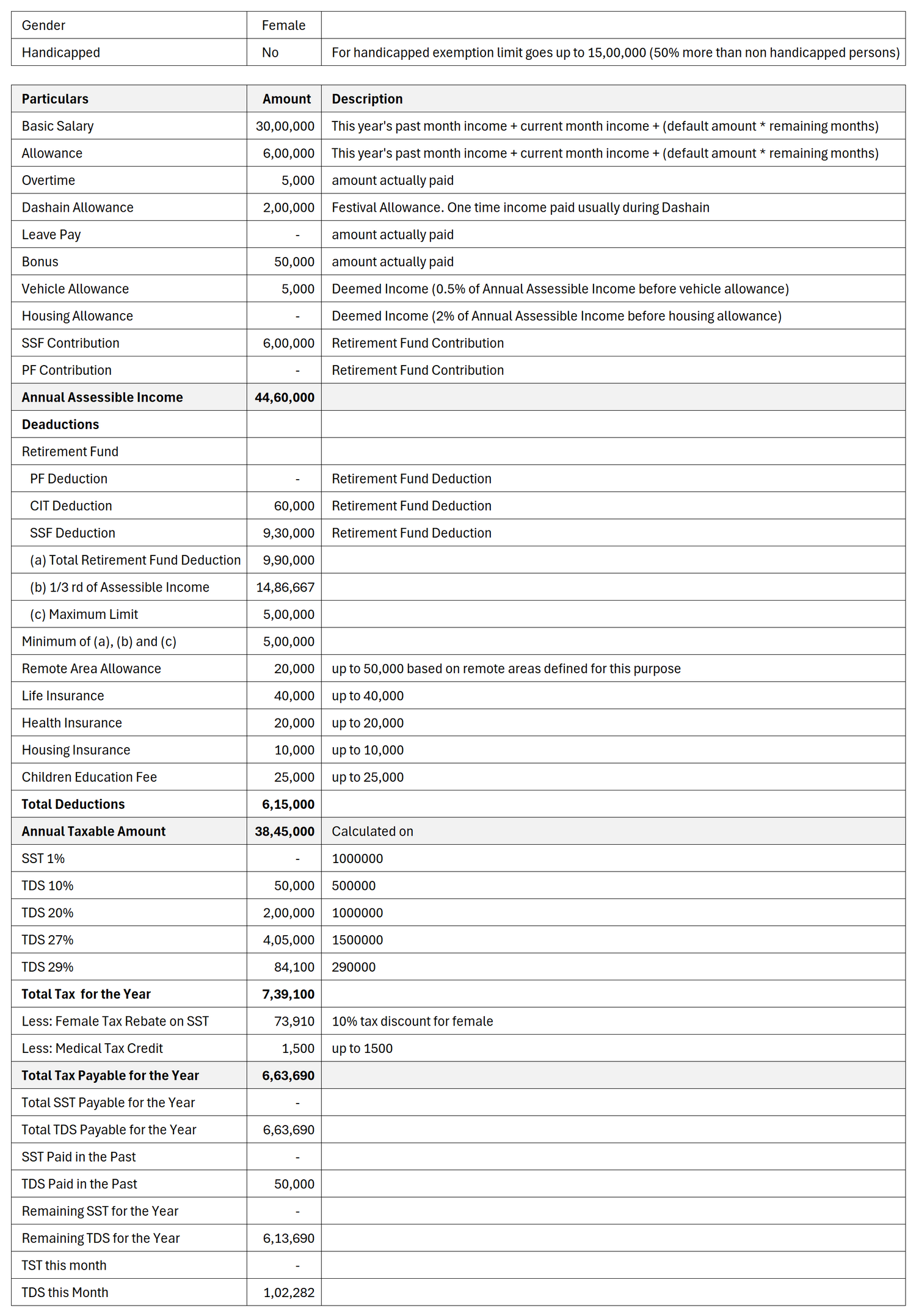

Your income is estimated for the whole year based on your current income and supplied information known at beginning of the year and is regularly updated when there are changes or new information is available throughout the year. For example, if you receive Rs. 50,000 salary in Shrawan 2083, your annual income will be estimated at Rs. 50,000 per month for 12 months in the year ie. (50,000 * 12) = Rs. 6,00,000. And later if your salary increases to 60,000 from Magh, the income is updated as 50,000 for 6 months and 60,000 for 6 months and it will become (50,000*6 + 60,000*6) = Rs. 7,60,000.

Sometimes there may be some additional incomes like Dashain Allowance. You may include such predictable income from the beginning of the year or add to your income when you receive it. If you add such income from the beginning of the year assuming that you are highly likely to receive it – your tax will be somewhat uniform throughout the year. And if you add such income as and when you receive it (like from the month of Ashawin), then your tax will be more in the later months and less in the early months. You may also choose to pay the tax on such irregular incomes fully when you receive it. The policy mostly depends on your organization’s decision rather than your individual decision.

Further, there may be some unpredictable incomes like Bonus, Overtime and some special allowances received in a month which may or may not be received in another month. Such types of incomes are added to your income when you receive them, and it will make your tax fluctuate from period to period. Your employer may choose to tax such incomes fully on payment or distribute the tax throughout the year.

Here is an example for tax calculation.

You can view and download your tax calculation details from RigoHR

How to calculate tax for Single or Couples

For the Financial Year 2083-84 (Shrawan 2083 – Ashadh 2084), whether you are single or married (previously single tax status or couple tax status) does not matter. You have the same tax exemption limit whether you are single or married.

Your income is taxable for year 3083-84 as per the following tax rates:

| Income | Tax Rate |

| Up to 10,00,000 | 1% (SST) |

| Next 5,00,000 | 10% (TDS) |

| Next 10,00,000 | 20% (TDS) |

| Next 15,00,000 | 27% (TDS) |

| More than 40,00,000 | 29% (TDS) |

For employees with disabilities the initial exemption of 10,00,000 is raised by another 50%. That means for employees with disabilities, the initial exemption limit becomes 15,00,000.

You do not need to pay 1% Social Security Tax if you are contributing to Social Security Fund (SSF).

What is Taxable Income?

Any income you receive from your employer (like salary, allowance, overtime, bonus) is taxable income. And any value you receive from your employer is also taxable even if you do not receive real money for that value you receive.

Examples of Taxable and Not Taxable Payments

| Salary | Taxable |

| Allowance | Taxable |

| Overtime | Taxable |

| Dashain Allowance | Taxable |

| Bonus | Taxable |

| Business Expenses Reimbursement (like travel expenses) | Not Taxable |

| Your company gives you house to stay. Not taxable for security guards or those types of employees who needs to stay at the office/factory premises due to their nature or work. | Taxable (@2% of your assessable income) |

| Your company provides car for your personal or personal and office use. If the car is provided only office use, it is not taxable | Taxable @0.5% of your assessable income |

In some cases, facility you receive are also included in your taxable income even if you do not receive any money for that. They are called deemed incomes.

Examples of Taxable Facilities/Deemed Incomes

| House provided by company to stay Not taxable for security guards or those types of employees who needs to stay at the office/factory premises due to their nature or work. | 2% of your annual income |

| Vehicle (car, jeep) provided by company for personal use or partially personal and partially official use not taxable is the vehicle is provided for office only use | 0.5% of your annual income |

| Any other facility | Estimated value of the facility you receive |

What you can deduct from Taxable Income

There are certain things that you can deduct from your annual income to determine taxable income.

1. Retirement Fund Contributions

If your company has contributed to SSF, CIT or PF, you can deduct up to 5 lakhs for retirement fund contributions.

The maximum limit for deduction is Rs. 5 Lakh.

How the amount is determined.

Let’s say your annual taxable income before retirement fund contributions is Rs. 21,00,000

- Your annual taxable income before retirement fund contributions is divided by 3. This comes to 21,00,000 / 3 = 7,00,000

- Your actual retirement fund contributions (sum of SSF, CIT and PF). Let’s say it is 4,00,000

- Maximum Limit is 5,00,000.

- Now you have to calculate the minimum of (a), (b) and (c). MIN (7,00,000, 4,00,000 and 5,00,000) is 4,00,000. Therefore, you can deduct 4,00,000 from annual income as retirement fund contributions.

RigoHR automatically does this for you. You do not need to do anything yourself.

2. Premium paid for Health, Life and Housing Insurance

If you have health, life or housing insurance (the house should be in your own name), you can deduct certain amount against the premium paid.

- Life Insurance: Up to 40,000

- Health Insurance: Up to 20,000

- Housing Insurance: Up to 10,000

You can submit your insurance record/proof of premium payment from RigoHR mobile app.

3. Charity and Donation

Charity and donation provided to eligible institutions can be deducted but up to a maximum limit of 3,00,000 or 5% of adjusted taxable income.

4. Remote Area Allowance

If you have worked in Remote Areas as specified by the government, you can deduct up to 50,000 based on the place you have worked in the year.

| Category | Deduction Amount |

| Ka | 50,000 |

| Kha | 40,000 |

| Ga | 30,000 |

| Gha | 20,000 |

| Nga | 10,000 |

5. Children Education Fee

There has been a new type of deduction from current financial year. If you have paid for your children’s education, you can deduct up to 25% of the amount paid in the year up to a maximum amount of Rs. 25,000. For that you have to submit the proof and request your HR department.

You can add your children education fee from RigoHR Mobile App.

Deduction from Tax

After your tax has been calculated by including your incomes and deductions stated above, you can directly deduct the calculated tax for the following:

1. Medical Tax Credit

If you have paid for you health treatment from approved hospitals or institutions, you can deduct up to Rs. 1,500 or 15% of the expenses you paid for such treatment. But if you have claimed Health Insurance Deduction, you cannot claim Medical Tax Credit. If you have health insurance, it is beneficial to claim health insurance deduction.

2. Female Tax Rebate

For female employees, you can deduct 10% of the total tax payable by you. Total tax includes both SST and TDS.

RigoHR automatically deducts 10% tax if you are female.

How the Tax is paid throughout the year

As mentioned above, your salary tax is calculated on your annual salary income (actual and estimated) reduced by any applicable deduction at the rates based on your income slab.

The total annual tax is divided by the total remaining months in the year. For example, if your annual tax is 60,000, you need to distribute that tax over the year and pay a monthly tax of 60,000 / 12 = 5,000. But this monthly tax may be different in the future months if there is change in incomes, deductions or any other tax information.

RigoHR automatically adjusts your income and taxes for all those factors.

Filing your Income Tax Return

For most of the employees, there is no need to file income tax return. Filing income tax return means filling D-03 form and getting tax certificate from Inland Revenue Department.

You do not need to file your income tax return if:

- You have income from salary only

- You have worked in one company at a time during the year (if you leave one company and join another company – it is ok, it is counted as one company at a time. But if you have worked in more than one company at the same time, you should file return)

- Charity and Donation deduction – not claimed

- Your annual taxable income is less than 40,00,000

Important note: If your annual taxable income is more than 40,00,000, you should file tax return and obtain tax clearance certificate in all cases.

Disclaimer: This article is not intended for legal advice. This article covers common cases only. There are many other conditions that can determine how your tax is calculation. For details refer to Income Tax Act. For easy reading, you can also refer to Income Tax Directive in IRD website